In the world of finance, challenger banks are the startups that decided to become Netflix in a world of blockbusters. Traditional banks, with their labyrinthine processes and penchant for paperwork, have long frustrated customers accustomed to instant results. It’s a little like using a rotary phone in the age of smartphones—a relic of another era.

The banking sector, while integral to modern economies, has historically been slower to adopt technological advancements than industries like e-commerce or media. Challenger banks, however, are changing that narrative. They’ve sidestepped the red tape and inertia that shackles traditional banks to create a fresh approach to financial services: no queues, no dusty branches, just seamless mobile apps and competitive services.

If you’ve ever marveled at the efficiency of blockchain for cutting out middlemen, you’ll understand the disruptive appeal of challenger banks. They leverage the same ethos of decentralization and innovation to bypass the bureaucracy that has defined banking for decades. And just like crypto reshaped digital ownership, challenger banks are reshaping financial services.

But what sets these institutions apart, and how can you create your own? Let’s explore.

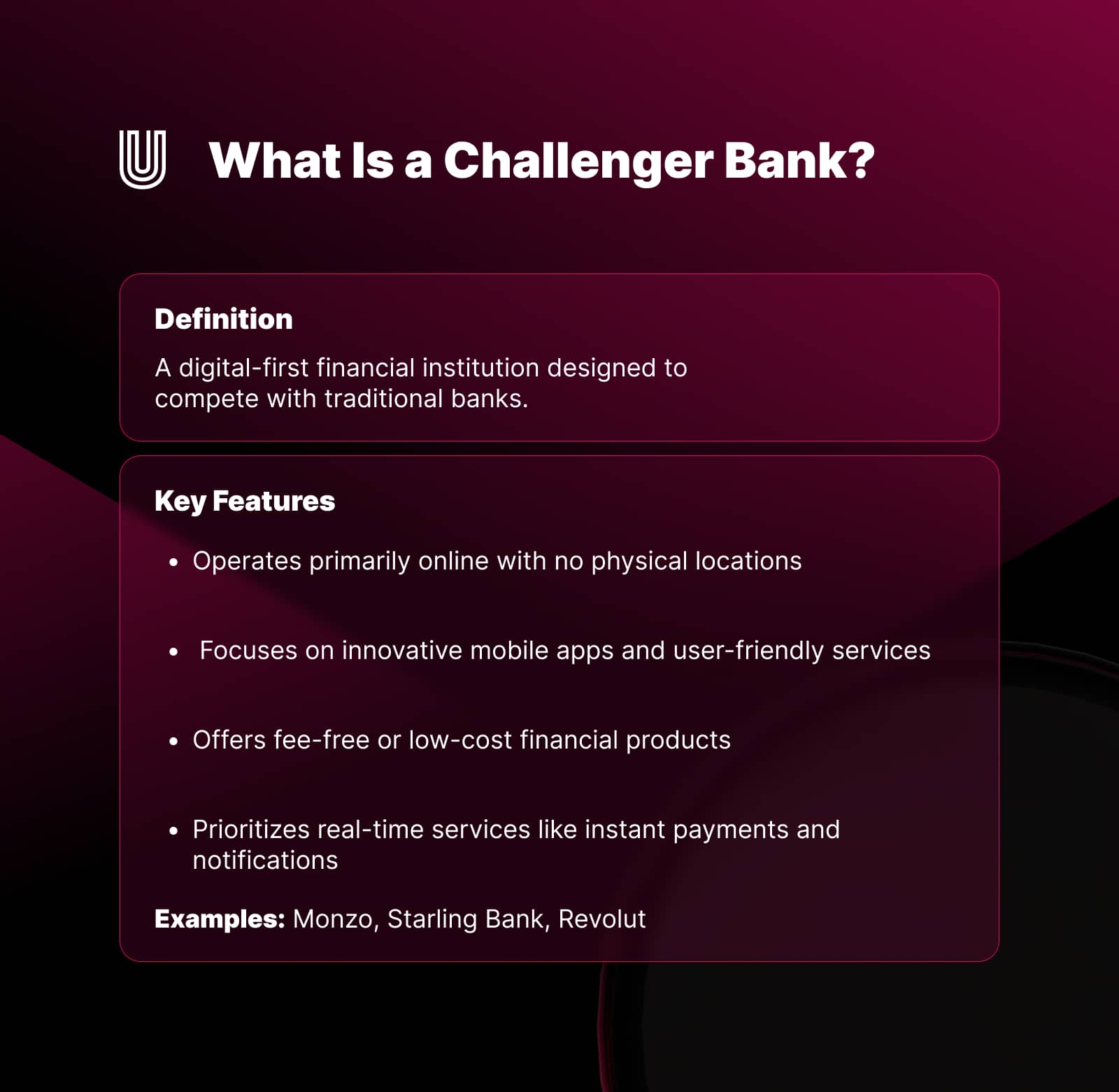

What Is a Challenger Bank?

Definition and Characteristics

Imagine you’re tired of waiting hours for a traditional bank transfer to clear while managing your digital assets on a blockchain wallet that settles transactions in minutes. Challenger banks are the financial industry’s answer to this inefficiency—a modern, streamlined approach that prioritizes technology and user experience over legacy systems.

A challenger bank is a digital-first financial institution that seeks to challenge the dominance of traditional banks. Unlike their older counterparts, these banks often have no physical locations, instead operating entirely through mobile apps and online platforms. This digital-native approach allows them to offer lower fees, faster services, and user-friendly interfaces that appeal to tech-savvy generations.

What sets challenger banks apart is their agility. They adapt to trends and consumer demands at the speed of a startup, launching innovative services like instant notifications for spending, integrated budgeting tools, and even fee-free international transfers. Think of them as the “smart contracts” of the banking sector—efficient, automated, and built for a user-centric world.

Historical Context

Challenger banks didn’t just appear overnight—they’re the product of a perfect storm of regulation, technology, and customer dissatisfaction. After the 2008 financial crisis exposed cracks in the banking sector, governments sought to diversify the financial landscape. In the UK, this led to the creation of the Prudential Regulation Authority (PRA) and the introduction of the Financial Services Act 2012, which paved the way for new banks to enter the market.

The UK’s 2018 implementation of the Payment Services Directive (PSD2) and Open Banking further accelerated the rise of challenger banks. These regulations required traditional banks to open their APIs, allowing third-party providers (including challengers) to access customer data with their consent. It was as if the walled garden of traditional banking had been pried open, creating fertile ground for disruption.

Metro Bank, the first challenger bank to receive a license in the UK in over 100 years, became the poster child for this movement in 2010. Soon, others followed—Starling, Monzo, and Revolut—each with a unique spin on what banking should look like in the digital age. While the term “challenger bank” originated in the UK, the phenomenon has since gone global, with neobanks and digital-first players gaining traction across Europe, the US, and beyond.

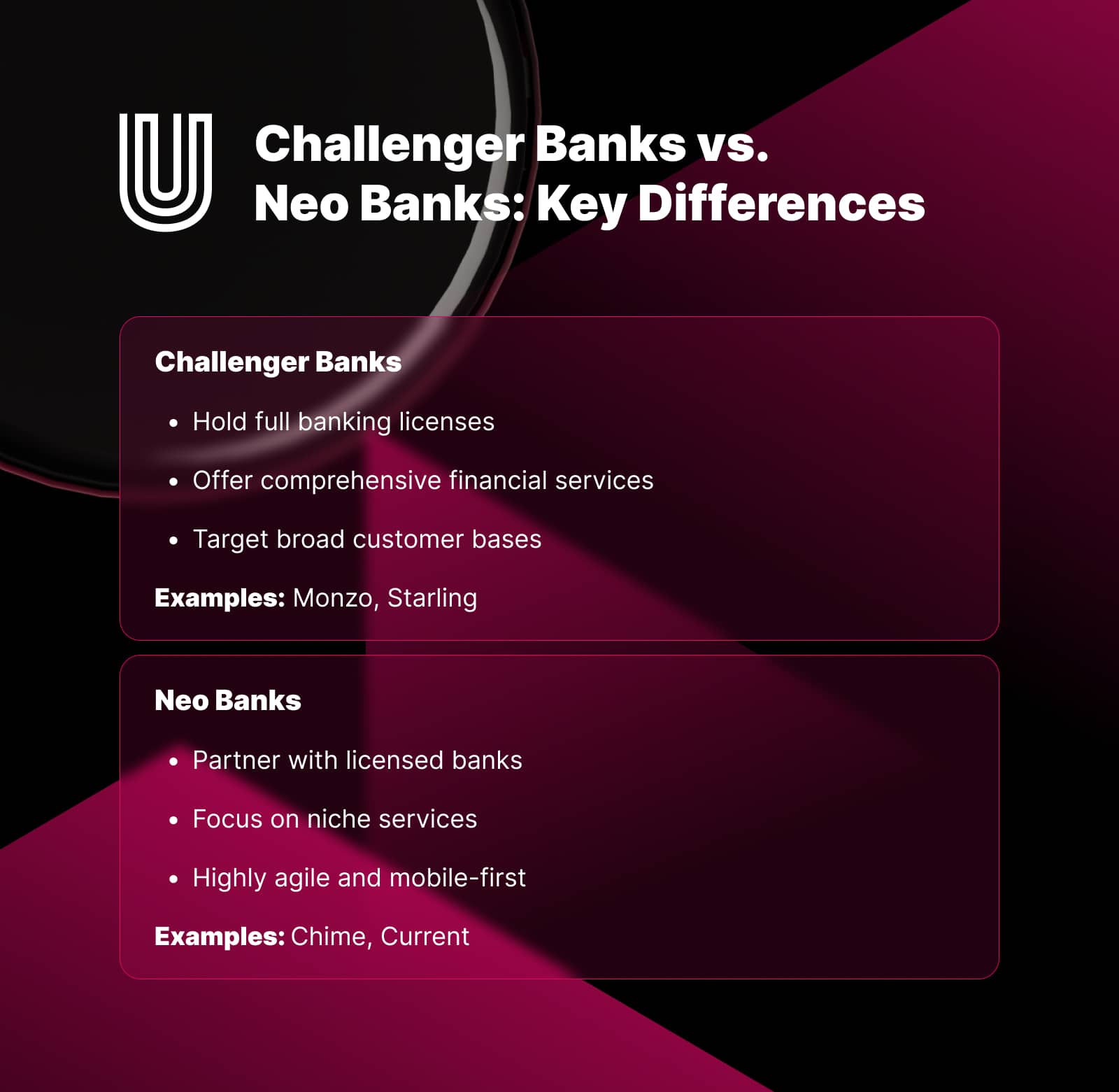

Challenger Banks vs. Neobanks

Key Differences

If challenger banks are the Robin Hoods of the financial world, neobanks are their minimalist cousins who operate entirely in the digital realm. While the terms are often used interchangeably, there are subtle but important distinctions between the two.

Challenger banks typically hold full banking licenses, which means they can offer a wide range of financial services directly, including loans, savings accounts, and debit cards. They’re built to disrupt the market from within, using the same regulatory frameworks as traditional banks but with a tech-first approach. Think of them as a Tesla—adopting the rules of the road but reimagining how the car is made.

Neobanks, on the other hand, are more like Uber—operating without owning the traditional infrastructure. They often partner with licensed financial institutions to provide their services, allowing them to focus exclusively on creating a slick, user-friendly digital experience. While neobanks may lack the regulatory independence of challenger banks, their agility and low overhead costs make them highly competitive.

For example, Starling Bank is a challenger bank that holds a full banking license, while Chime, a neobank in the US, partners with The Bancorp Bank to provide its services. Both appeal to tech-savvy consumers, but the structural differences influence how they operate and scale.

Pros and Cons

The choice between challenger banks and neobanks often comes down to priorities—are you looking for a tech-savvy disruptor with regulatory clout or an ultra-lean digital experience provider?

Challenger Banks:

• Pros:

• Full banking license enables a comprehensive suite of services.

• Greater trust due to regulatory compliance and financial protections.

• Scalability and longevity due to independent operations.

• Cons:

• Higher setup and operating costs compared to neobanks.

• Slower innovation cycles due to regulatory constraints.

Neobanks:

• Pros:

• Low operational costs allow for competitive pricing (e.g., no monthly fees).

• Rapid feature deployment and updates.

• Focused solely on user experience.

• Cons:

• Dependence on third-party providers limits independence.

• Restricted service offerings compared to fully licensed banks.

Ultimately, while the lines between challenger banks and neobanks continue to blur, understanding these nuances helps entrepreneurs and consumers make informed decisions.

The Growth of Challenger Banks in the Banking Sector

Market Trends and Statistics

Challenger banks have significantly reshaped the financial services landscape, offering digital-first solutions that attract a growing number of consumers worldwide. The global neo and challenger bank market was valued at approximately USD 118.01 billion in 2023 and is projected to reach USD 2,597.03 billion by 2031, growing at a compound annual growth rate (CAGR) of 47.17% during the forecast period (Verified Market Research).

In the United Kingdom, the birthplace of many challenger banks, institutions like Monzo, Starling, and Revolut have experienced substantial growth. Monzo, for instance, reported an increase from 7.4 million customers in 2023 to approximately 9.7 million in 2024 (Statista).

Revolut, another prominent UK-based challenger bank, reported a significant increase in revenue, reaching £1.8 billion in 2023, nearly doubling from the previous year. This growth was driven by higher interest rates and an expanding customer base, with the company achieving a pre-tax profit of £437.8 million, a substantial turnaround from a £25.4 million loss in 2022 (The Times).

In Latin America, Brazil’s Nubank has demonstrated remarkable customer acquisition, reaching 93 million customers by December 2023, reflecting the growing demand for digital banking services in the region (Statista).

These trends underscore the increasing consumer demand for digital banking solutions that offer convenience, transparency, and user-friendly interfaces, challenging traditional banking models and prompting a global shift toward digital financial services.

Case Studies

The success of challenger banks is exemplified by several key players that have leveraged technology to meet evolving consumer needs:

• Monzo: A UK-based digital bank known for its user-friendly mobile application, Monzo has seen significant growth, reaching approximately 9.7 million customers in 2024, up from 7.4 million in 2023 (Statista).

• Revolut: Operating on a global scale, Revolut offers a range of services including multi-currency accounts and cryptocurrency trading. In 2023, the company reported revenues of £1.8 billion and a pre-tax profit of £437.8 million, marking a significant turnaround from the previous year’s loss (The Times).

• Nubank: Based in Brazil, Nubank has rapidly expanded its customer base, reaching 93 million customers by December 2023, demonstrating the growing demand for digital banking services in Latin America (Statista).

These institutions illustrate how challenger banks are effectively meeting the demand for innovative, customer-centric banking solutions, leading to substantial growth and disrupting traditional banking paradigms.

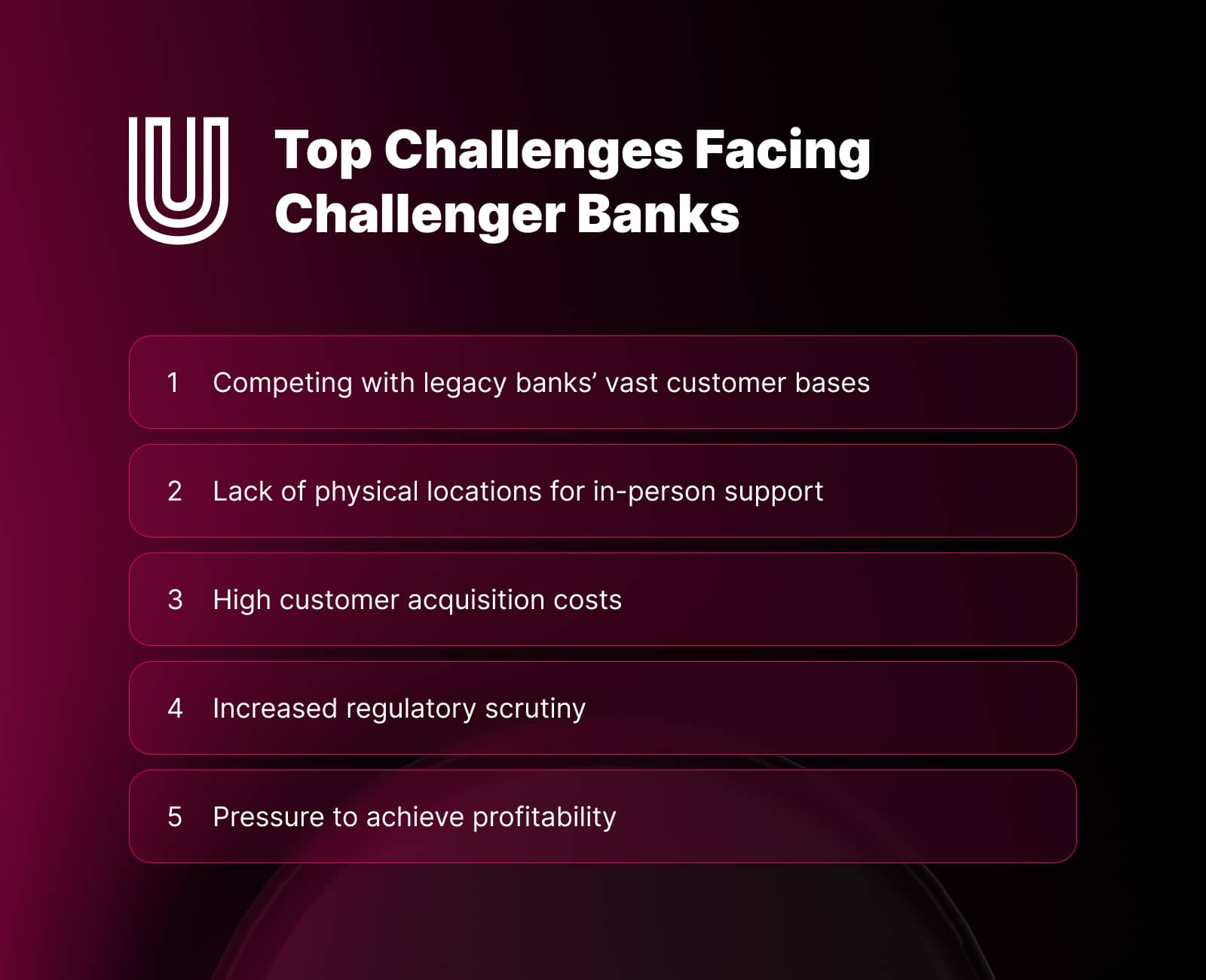

Challenges Facing Challenger Banks

Competition with Traditional Banks

Traditional banks are enhancing their digital offerings to compete with challenger banks. Legacy banks are adopting advanced technologies to improve customer experience and operational efficiency. Additionally, the extensive network of physical locations that traditional banks maintain remains an advantage, providing a hybrid experience that digital-only neo banks cannot replicate.

While challenger banks focus on digital innovation, traditional institutions leverage their reputation, bundling services like mortgages, loans, and insurance, which challengers often struggle to match. For many consumers, familiarity with established brands and the convenience of in-person services continue to be compelling reasons to stay with legacy banks.

Sustainability and Profitability

Achieving sustainability and profitability remains a significant hurdle for challenger banks. While some, like Revolut, have reported profits, others continue to prioritize growth over profitability, leading to high operational costs and reliance on external funding. Analysts suggest that long-term success will require a stronger focus on operational efficiency and scaling effectively.

Regulatory scrutiny is another ongoing challenge. Many neo banks face increasing compliance costs, particularly in areas like cybersecurity and anti-money laundering protocols. These added expenses can weigh heavily on their already thin margins. The absence of physical locations might reduce overheads, but it also limits opportunities for face-to-face customer interactions in regions where personal connections remain important.

Future Outlook for Challenger Banks

Emerging Trends

Challenger banks are driving innovation by adopting artificial intelligence (AI) and machine learning to enhance customer service, fraud detection, and credit scoring. These technologies allow banks to offer personalized experiences while improving operational efficiency.

The rise of embedded finance—integrating financial services directly into non-financial platforms—represents another opportunity for challenger banks. Partnerships with companies like Shopify or Uber enable them to expand their reach without the need for significant infrastructure investments. Additionally, sustainability-focused banking is becoming more prevalent, with neo banks offering green financial products and aligning with Environmental, Social, and Governance (ESG) principles to attract eco-conscious customers.

Potential Opportunities and Threats

The global expansion of challenger banks presents enormous opportunities, particularly in underserved regions. By leveraging digital platforms, neo banks can tap into markets where traditional banking infrastructure is underdeveloped. However, this expansion requires navigating complex regulatory environments, which can be costly and time-intensive.

At the same time, profitability continues to be a major challenge. Many challenger banks struggle to retain customers who often switch platforms for better deals. Additionally, the looming presence of Big Tech—companies like Apple and Google entering financial services—poses a significant competitive threat, given their extensive resources and user bases.

The Role of Challenger Banks in the Future of Banking

Challenger banks, including neo banks, represent a paradigm shift in how financial services are delivered. By leveraging technology and addressing inefficiencies in traditional banking systems, they have redefined customer expectations. Their innovations, such as real-time spending notifications and fee-free international transactions, have forced legacy institutions to modernize their offerings.

The absence of physical locations allows challenger banks to operate with lower overheads, enabling them to offer competitive pricing. However, this digital-only approach also limits customer engagement in markets where personal service is still valued.

Ultimately, the success of challenger banks lies in their ability to balance innovation with financial stability. By addressing underserved demographics and redefining traditional banking models, they are shaping a more inclusive and dynamic financial ecosystem.

Frequently asked questions

What Are Challenger Banks and How Do They Work?

Challenger banks are digital-first financial institutions designed to compete with traditional banks by offering innovative, user-friendly services. They typically operate online without physical locations, focusing on mobile apps and digital platforms. By leveraging advanced technology, challenger banks provide features like real-time spending notifications, fee-free international transfers, and budgeting tools.

How Do Challenger Banks Differ from Neo Banks?

While the terms are often used interchangeably, challenger banks typically hold full banking licenses, enabling them to offer a wide range of financial services directly. Neo banks, on the other hand, often rely on partnerships with licensed institutions to provide their services. Both focus on mobile-first solutions, but challenger banks may have broader offerings, whereas neo banks are more agile and niche-focused.

Are Challenger Banks Safe to Use Compared to Traditional Banks?

Yes, challenger banks are generally safe to use, as they are regulated by the same authorities overseeing traditional banks, such as the FCA in the UK. Many also offer deposit protection schemes, safeguarding customer funds up to a certain limit. However, users should verify that the bank holds the necessary licenses and complies with regulations to ensure their money is secure.